After 8 man/months of effort, we have finally released the 52 page Populous 2.0 report.

|

|

|

This report was updated multiple times after being flagged for various deficiencies. Download the Populous Forensic Valuation and Analysis 2.0 - Public Edition, and feel free to comment via the comment section below.

A PayPie report that is even more in depth than this one is planned for release next week. That will be for VERI token holders only. This public version does not have the valuation bands, but HODLers of VERI tokens can purchase them for the equivalent of $500 US in VERI.

Comments

Based on my understanding of the report and prior research on Populous, this is what I believe is the vision of Populous. I haven't quite seen it in this context. This is my 0.02 cents (2 satoshis).

First off, in my humble opinion Populous is a disruptive company. It is an ambitious project that is starting with invoices and may extend to home loans. It's still new and will need the brightest minds to bring to life.

If Populous delivers their vision, they may end up creating one of the most valuable financial protocols ever seen on this planet.

PPT is positioning itself to benefit the general public via decentralized p2p lending.

What is our current monetary system? USD is in essence Debt (issued by the government).

PPT is using a hybrid of debt and Gold bullion to establish store of value which will become a dominant tradable exchange currency. There will be many value exchange currencies depending on the utility.

What is the PPT token backed by?

1. Trust in its decentralized nature

2. Gold reserves

3. Debt / Corporate/Bank/Vendor invoices.

The year is 2022.

John Deere needs a short term loan via the invoices he receives from his vendors. John needs new heavy equipment for his company.

1. John goes to the Populous site, verifies his information, and posts his invoice looking for investors. The invoice (a debt instrument) pays out in 45 days.

2. Jenny the Investor is a PPT holder. Jenny goes to Populous site to invest in an invoice. She finds John's invoice listing offer and jumps in on the auction. Jenny invested in PPT in 2017 because she wanted additional cash flow during retirement.

2. Jenny deposits 100 PPT into Populous' decentralized smart contract using her mobile phone crypto wallet.

3. The Populous smart contract automatically calculates the local fiat currency value of PPT value (from the PPT 30-day moving average).

4. John sees that his invoice got funded. He sees a digital token called pUSD sent to his wallet. He is happy because the digital token is a gold backed fiat token that he can spend towards his business expenses.

5. John Deere is happy. He can now pay his employees and get his heavy equipment to finish the job on the invoice.

- John Deere is confidence because the Populous pUSD poken is more stable than actual fiat dollars. It is also more trusted than the USD Tether token. The pUSD poken is digital and and easy to send around.

6. John Deere pays his employees, vendors, contractors, building leases in digital pUSD gold backed pokens.

7. The employees love these pokens because they are accepted all over the internet.

8. John Deere pays his vendor in pUSD pokens. John Deere also pays his lease in pUSD. The gold backed token is accepted all around the world.

9. After 45 days John Deere's invoice is paid back to Populous. Populous smart contract receives the USD fiat digitally and releases PPT back to Jenny.

10. Jenny the Investor comes back next month with her PPT to do it again.

The topic of a dual token model is interesting to me because it is a common problem. The reason why you can't have a single-token model is because you simply can't get the level of liquidity needed to maintain a stable value. If there was a big afternoon wherein several million dollars of invoices were sold and the invoice sellers received PPT tokens that they'd have to turn around and sell, it would put serious price pressure on the token price, and that would threaten the economics of the whole system. You could use DAI or Tether, but they would have to have sufficient liquidity to handle the volume of transactions as well, and we all know the purported risks in USDT.

The use of gold confuses me, and I agree with Reggie's statements. The problem with buying and selling physical gold is that the spread is usually significant and will eat margins and for what benefit? The only thing I can see here is that I'm guessing when the business reaches steady state operations they'd only be transacting a fraction of the gold holdings - the net gain/loss required.

The problem I have is that the whole platform relies on PPT having enough in the liquidity pool to buy pokens that the invoice sellers are selling. They raised roughly $10M in ICO as I recall. The ETH might still be worth that, maybe $20M. PPT supposedly has a deal to borrow fiat at rates such as 0.5%/month, but this arrangement seems sketchy but I understand why they can't talk about it more. $10M or $20M is not nearly enough.

The Distributed Ledger Technology (DLT) seemed to originally be for everybody, including the small guy. But, that original idea appears to have been lost and the players in the blockchain sectors appear to mostly have the same MIND set as the legacy bloodsuckers...perhaps, that is because they feel the necessity to jump through the hoops of regulations and laws that have no place in a peer-to-peer economy. I could rant my opinion more...but, I will not do that right now.

I REALLY liked the idea of invoice factoring disintermediation. However, the idea of AUCTION from the Populous model will only drive the prices up for these business that need cash. That is no bueno. GREED is a factor that exists in legacy banking AND this cryptoworld. We need to fix that or, this DLT experiment is DOOMED!

A set standard/yield could be set.

One of the "competitors" is geared for INSTITUTIONAL Investors only?!?! Again, the point is being lost. That is like ONLY allowing accredited investors to participate.

I plan to add more once I finish the report. The BEST part of the Populous report is the brilliant work of the Vertaseum team...the opportunity to add input on this forum could add to helping the GREAT idea of Populous to be refined more for optimum success.

That depends on WHO is doing the bidding? I have personally witnessed prices skyrocketed in auction settings.

Perhaps, the SME's could be given a SET rate. that could eliminate the potential for problems and allow for the smart contracts to automate more easily.

I am just speaking to the benefit of the regular people. They are the ones that NEED financial knowledge and opportunity. That is MOST important for the world to change.

The REGULATORS should spend LESS time trying to control this new technology and freedom ...and MORE time and money implementing financial EDUCATION and LITERACY knowledge and course! The BIG guys and girls in crypto should campaign for THAT to be implemented. Don't just stand by and allow them to regulate your freedoms away!

Instead of BLAME the guilty parties, let's produce the KNOWLEDGE for the regular people! I am willing to help 100% in that effort.

Back to the instant topic:

The retail investor is not the enemy...but, they have been scapegoated into that class (I guess).

I have NOT seen any regulations for title 15 section 78 (as well as other code sections), but I have to study more thoroughly, and, I am not an attorney.

Just wanted to add this comment. Still have to complete the Populous report. Doing that tonight.

All the best.

I did. Your team omitted the biggest competitor in their report. When you read the Debitum white paper you will see in their own analysis that PPT is their competitor.

"The entire industry is old school, so that is not legitimate criticism of gold as a backing. I'm not in favor of gold backing due to its illiquidity and friction."

And I'm not a fan due to ease of fraud. And more importantly, trust issues, which if blockchain doesn't completely erase makes the product nothing more than a database. Trust issue, Reggie.

"As consultants, I feel we would be able to provide a better solution." We already have. I believe that Debitum is a good competitor and your researchers should have included a review of it as a competitor in the report.

Debitum targets the loan market for SMEs, a niche that Populous is also targeting. Populous say that they use a proprietary Altman Z score credit rating. Because it's proprietary, they can't reveal it for analysis. Nor are they able to show a history of success in using their credit score. There are a number of things that niggle me about PPT but I'm as super hyped on Debitum as much as I am on Veritaseum, as you know. (This messaging is really slow and I can't tell if my messages are not going through or are being edited out. Sorry if I repeat myself in messages.)

Does Debitum plan to focus on the UK for the first 2 to 5 years - or greater Europe?

Altman Z scores are easily found in the public domain. The proprietary nature is likely more related to XBRL than the Z score. In addition, Populous does not have to reveal their credit rating system for analysis, no other company does.

Can you illustrate the history of success of other successful credit scoring agencies?

We critiqued what we knew, and gave management ample time to address what we didn't know and we published thier responses.

The loans are to be made in cash, but deals settled in tokens.

Just seems so many multiple layers of complexity & uncertainty - gold, ETH, pokens, tokens - all subject to price change. Seems like an obstacle.

During Reggie's recent interview, I did think to ask what Reggie&team might have suggested were they consulted.

I see the DAI token has set out to achieve price stability and is just about achieving it.

The loans are to be made in cash, but deals settled in tokens.

Just seems so many multiple layers of complexity & uncertainty - gold, ETH, pokens, tokens - all subject to price change. Seems like an obstacle.

During Reggie's recent interview, I did think to ask what Reggie&team might have suggested were they consulted.

I see the DAI token token has set out to achieve price stability and is just about achieving it.

I'm not sure Debitum is direct competitor, review the research document. The entire industry is old school, so that is not legitimate criticism of gold as a backing. I'm not in favor of gold backing due to its illiquidity and friction.

As consultants, I feel we would be able to provide a better solution.

Hi Reggie. Happy Easter! We love you! It's me, Earthy from Austin, Texas. Reggie, the fact that your team omitted Debitum as a viable competitor in your report is a shortfall on their part. Debitum is directly targeting the Populous market for small and medium sized businesses. Plus these people already have successful businesses in IT and financing. And they are converting from fiat as necessary which will eventually become interoperable cryptos. That's the model. Trusting in gold backing which is open to abuse is very short-sighted. Plus why confuse the issue by issuing PPT and then Pokens. Also there was no mention that their "proprietary" credit risk rating is just the Altman Z score. What's so proprietary about that?

I know you have not read Debitum's excellent white paper which lists Populous as a direct competitor. Check out Debitum, Reggie.

Also please give me contractor access as already requested. I need to learn the ropes of your platform so I can help you help me make lots of money.

I would have to disagree with you Earthy. The fact that Vertitaseum has produced a report on a company that it admits it does not fully understand, I deem as being irresponsible. Competition IS fierce and a company like Populous that has not 1 but 2 patents pending has purposely chosen to withhold information. They should not be penalized for protecting their ground breaking technology. To further prove my point, Gold is not being used soley as a means of conversion, nor will it require trust as you state. Populous has achieved a trustless platform by using the Blockchain ledgers and smart contracts. So, the fact that you state this shows me that you have been misguided by this report. Another comment above

was "I'm not in favor of gold backing due to its illiquidity and friction". This is the exact reason why Gold can be and will be used more and more; Gold is an absolute means of liquidity, can easily be recorded on a blockchain ledger, and when exchanged for fiat creates 0 friction. Get back to me when banks start closing down or freezing these start-up's fiat accounts. It is happening now and will only get worse as the Old Legacy system begin to feel threatened by the fintech/blockchain revolution. **I understand Reggie and wholeheartedly believe his has good intentions. The report was good in that it explained the Invoicing discounting marketplace but the report failed to give an accurate description of what Populous does or how it does it. How could it have without knowing the most intricate workings of the company? Imo, companies should be investigated and reported on after they launch. Creating a report that is filled with speculation and inaccuracies defeats the purpose.

Having patents pending has nothing to do with fleshing out the business plan. Patents pending are published by patent offices.

Recorded on a ledger and trustlessly tracked are two different things. It doesn't sound as if you have a firm grasp of the pros and cons of physical asset tokenization.

Your comments are, to be as politically correct as possible, inaccurate and way off point. Populous management was asked to clarify the points that we were not certain of, and we even went so far as to publish the questions and answers provided. We believe PPT is the current leader in this space, but they are not perfect, and the holes that we seem to have found in the business model/plan have not been filled as of yet.

I welcome PPT management to clear these issues here in the public discsussion. It is a tightly controlled environment where CEOs can speak openly and freely in a verbose fashion and do not have to worry about FUD and trolling, since we are quite familiar with that activity.

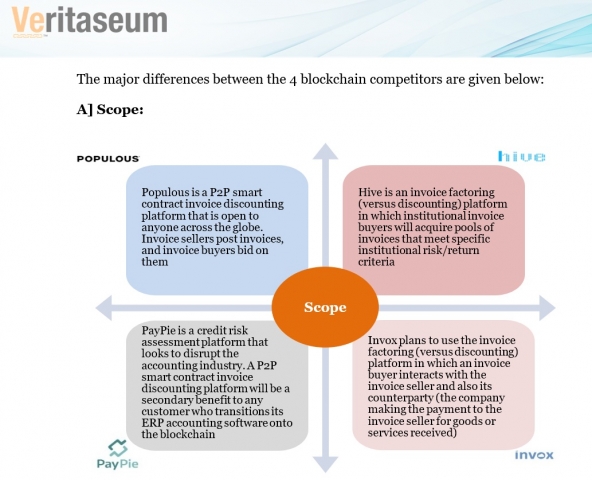

- The complexity of the token model. This is not specific to just Populous, for we feel that the other token-based invoice factoring and discount companies also use materially unnecessary levels of complexity to achieve what appears to be relatively simple goals. I invite the management of any and all of these companies to chime in on this - particularly those mentioned in the report: Hive, Populous, PayPie and Invox.

- Inability to source XBRL in markets outside of the UK

- The burning of tokens, will likely not result in an increase in intrinsic value.

I'll also make Veritaseum team analysts available for disussion as well.

In regards to the Populous report, I feel not enough attention was given to the critical sections. No company is perfect, and there are some parts of the business plans/model/operations that we either did not understand or do not pass muster. This is not to say that we are bearish on the company, but it is to say that we believe there is significantly more fleshing out of the model before PPT is ready for prime time. Either that or management is purposely leaving out some key details, possibly for strategic or competitive reasons.

Issues that I would like to discuss openly in this chat:

- Political instability will cause volatility in earnings & unpredictability in market penetration (BREXIT).

- PPT's competition are entrenched players than blockchain startups (whom all server different markets/segments)

RSS feed for comments to this post