This is an example of the level of analysis that our Veritas token holders can come to expect. The research will be available a la carte in exchange for Veritas tokens (VERI) until our financial machines are operational - after which all research will be available only through digital asset exposure of the machines.

See this video or Veritaseum found Reggie Middleton in a fireside chat with hedge fund managers at Citco corporate headquarters for a fuller explanation or Veritaseum's Peer-to-Peer Capital Assets business model.

We welcome one and all to compare and contrast our Veritas token-powered research with the best that the web has to offer. For the topic of Gnosis, we suggest you reference Token Market and Smith and Crown. Only We have an entire team of buy-side financial analysts, engineers and forensic accountants led by the globally renown investor and Veritaseum founder Reggie Middleton, focused specifically on the token, digital asset and ICO sector.,

Learn more about Veritaseum, go to purchase Veritas (VERI) tokens, or simply continue to read the best research on digital assets currently available.

-

GNOSIS Company Overview

-

Overview

Gnosis is providing a platform for the next generation of prediction markets. The platform is built on Ethereum. Users shall be able to forecast future events by using the platform and will be creating different events thereon. The platform works on a decentralized model which allows participants to place their predictions on an event, which then gets aggregated to form a collective view on prediction. In simple words, Gnosis attempts to create among other things a unique forecasting tool for people to render and receive projections for an event or result.

Besides this, it aims to create an ecosystem of customized information search wherein any person can post a question and fund search for the answer. The availability of unlimited resources creates a market for prediction, and the users as well as those participating in the prediction benefit for their intellect and knowledge.

The Company is attempting to create a smart contract universe to reward successful users for predicting the outcome correctly. The way in which Gnosis prediction works:

- An event is posted: “Would Brazil win the next Football World Cup?”

- User buys a position

- At the end of the event, the successful users’ shares will ‘get redeemed for $1 each. Losing users’ share will become worthless

Details of Gnosis Token

|

Tokens |

10 million fixed tokens (GNO) which generate WIZ. WIZ can be used to pay fees on the platform. Apparently, on 3.16% of the tokens were Dutch auctioned off for $12.5 million dollars |

|

Additional Tokens |

No additional tokens to be released, for at least a year (token lock-up period), although 10 million created |

|

Underlying Blockchain |

Ethereum |

|

Services |

Group into three layers of services : Layer 1 (Core), Layer 2 (Services) and Layer 3 (Applications) |

|

Model |

Decentralized prediction model |

-

Segment Analysis

-

Layer 1: Gnosis Core

The Core layer enables smart contracts for Gnosis use:

- Event Token Creation

- Settlement

- Market Mechanism

- Oracle

- Management Interface

These services will be free for use.

-

Layer 2: Gnosis Services

The Services Layer will offer trading fee model and additional services over the Gnosis Core.

- State Channel Implementation

- New Market Mechanisms,

- Stable Coin and Payment Processor Integrations,

- Open Source Template Applications,

- Application Customization Tools, and

- Oracle Marketplace

These services will attract a fee. Participants at Gnosis Core level will upgrade to this level of service due to wider potential applications, use cases and benefits.

-

Layer 3: Gnosis Applications

The Application Layer will target specific prediction market in areas like the following:

- Financial Instruments

- Insurance & Hedging Instruments

- Information Sales

- Governance

- Incentivization

- Sports Betting

These applications will attract additional fee or charges on the basis of market making, information selling, or advertising.

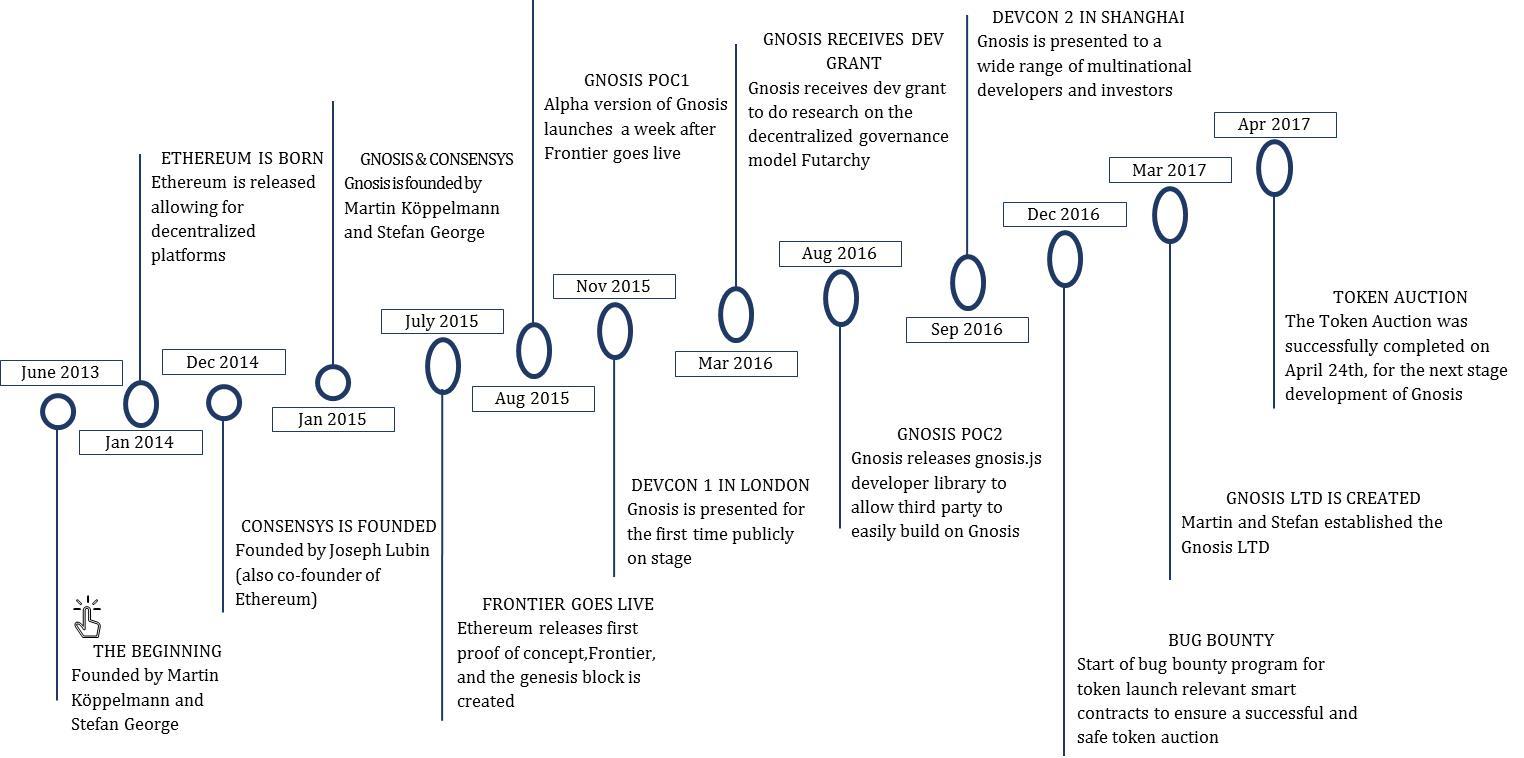

Company History

Aspects of Interest in the Time Line:

- In Jan, 2013 Martin Köppelmann and Stefan George created the largest Bitcoin Prediction Market,

- In Jan, 2014 Ethereum was Born,

- In Jan, 2015 Gnosis was founded by Martin Köppelmann and Stefan George,

- In July, 2015 Ethereum releases first proof of concept, Frontier

- In Nov, 2015 Gnosis was presented for the first time publicly on stage to the Ethereum developer community,

- In Sep, 2016 Gnosis was presented to a wide range of multinational developers and investors in Shanghai,

- In Mar, 2017 Gnosis LTD is established by Martin and Stefan,

- On 24th April, 2017 the Token auction was successfully completed, for the next stage of Gnosis development

-

Key Financials

-

Revenues

|

Revenues during 12 months (USD thousand) |

|

|

Gnosis is likely to derive the majority of its “operating” (more on this later) revenue from Layer 3 services in the latter months of the above 12 month period.

- Layer 3 will grow at a monthly growth rate of around 20% on account of direct sale and cross-selling of application services

- These services will garner more value per user and will, therefore, more impact on revenue growth

- Layer 2 services are also expected to have almost similar growth (~21%) but the value of these services per user as well as in total will be lower compared to that of Layer 3

- Layer 1 services will concentrate on customer expansion to cross-sell Layer 2 and Layer 3 services

-

Gross Profit

|

Gross Profit during 12 months (USD thousand) |

|

|

Gross margin of the Company is expected to widen on account of increase in the share of revenue from higher margin services in the total revenue.

- Layer 2 and Layer 3 services are assumed to have margin of 60% and 70%, respectively, compared to revenue of 10% gross margin for Layer 1

- Share of revenue from Layer 1 and Layer 2 services is reflected to reduce gradually in accordance with increase in revenue from Layer 3 services

-

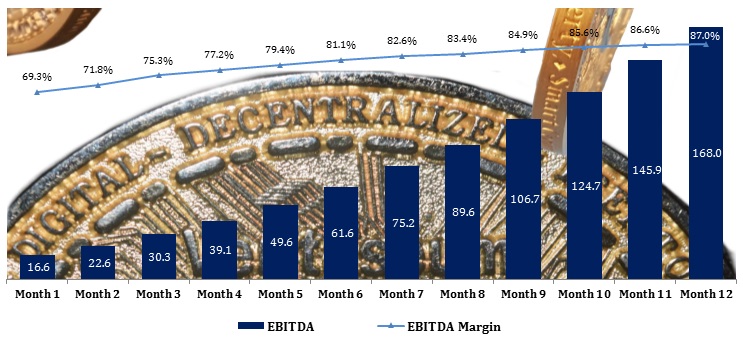

EBITDA

|

EBITDA during 12 months (USD thousand) |

|

|

Similar to the trend of gross margin, the EBITDA is expected to grow in line with the increase in the share of revenue from Layer 2 and Layer 3 services.

- EBITDA is projected to grow from $16.6 (thousands) to $168 (thousand) at a monthly grow rate of 21.3%

- EBITDA margin on Layer 2 and Layer 3 is approx. 80% (average) and 85% (average). Layer 1 EBITDA margin is 2.6% (almost break-even)

-

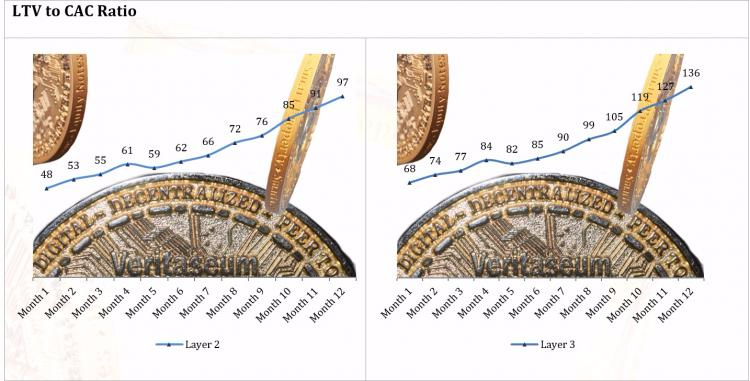

CAC and LTV and LTV/CAC

|

Customer Acquisition Cost (CAC) ($) |

|

|

|

|

|

Lifetime Value (LTV) ($) |

|

|

|

|

- Customer Acquisition Cost (CAC) is declining over the period of time. This is because the increase in a number of customers is greater than the increase in sales and marketing expenses. As the business matures, fewer expenses per customer acquisition are expected to incur

- Life Time Value (LTV) is gradually increasing as can be seen in the chart. This growth can be primarily attributed to a decrease in churn rate of revenue. Monthly recurring revenue churns out every month, the rate of which decreases over a period of time. This, in turn, increases the lifetime value of the customers

- LTV to CAC ratio shows an increasing trend as per the charts above. This is a healthy indicator for a business of this kind

-

Valuation

-

Valuation Methodology

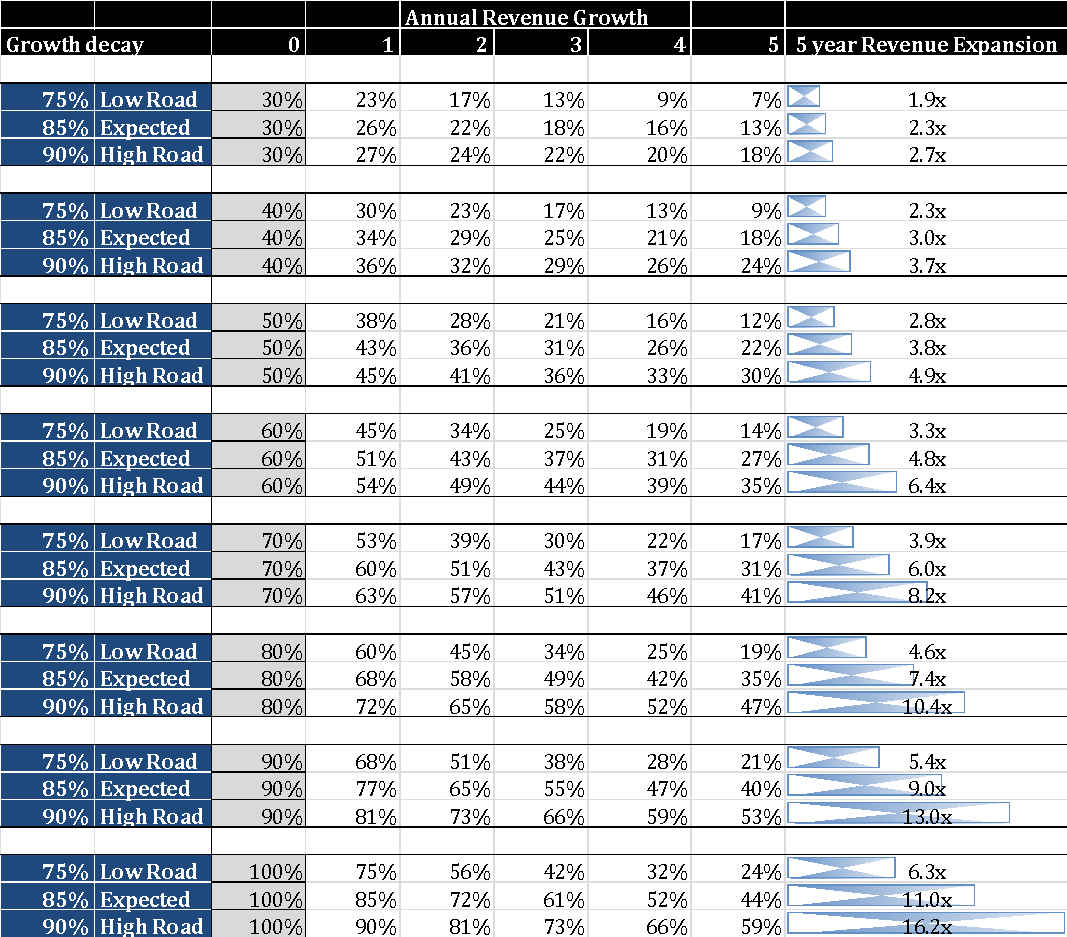

This exercise of analysis of valuation is being conducted in order to assess the fair value of Gnosis. We analyzed the fair valuation of Gnosis’ “operating” rrevenues in accordance with the Growth Rate Decay Trajectory method. The growth rates in new companies are generally very high in first two years; however, these growth rates decline relatively predictably as the companies mature. On a separate note, using relative valuation approach or Discounted Cash Flow approach will not give plausible results as they don’t account for longer term revenues and are sensitive to near-to-medium term cash flows. None of these methods fully capture the entire value-add of all three layers, though. This is our default valuation metric for blockchain-based platforms, and platform-centric application builders – with an addendum for token appreciation.

Following is the methodology for the valuation of Gnosis:

Growth Rate Decay Trajectory Method:

The Growth Rate Decay Trajectory method estimates the value of a business based on the current revenues and trailing revenue growth during the forecasted period.

The method is based on projected long-term trend in revenue without emphasizing on the near-to-medium term cash flows. This method is, therefore, ideal for a business that has potential to have multiplier growth in the longer run but burns through its cash flow in the short-to-medium term.

We have assumed the below mentioned growth paths forward:

- The Low Road - The growth rate decays and each year's growth rate is assumed to decay to 75% of the prior year's growth rate.

- The Expected Outcome - The growth rate decays to 85% of the prior year's growth rate.

- The High Road - The growth rate proves to be very persistent and is assumed to decay to 90% of the prior years.

Below table shows the three different growth paths for initial growth rates ranging from 30% to 100%:

The five year revenue expansion figure in the above table shows that a company should not decay at anything above the industry’s expected decay. Though the figures of growth decay may differ only slightly, their implication of 5 year revenues can be huge.

This 5 year expansion multiple is applied to the current revenue for valuation. This method is best suited for companies with the potential to have long term revenue (and expected to burn cash in the near-to-medium term) as against the Discounted Cash Flow and Relative Valuation Method.

Blockchain Ecosystem-specific Economic Revenue Recognition

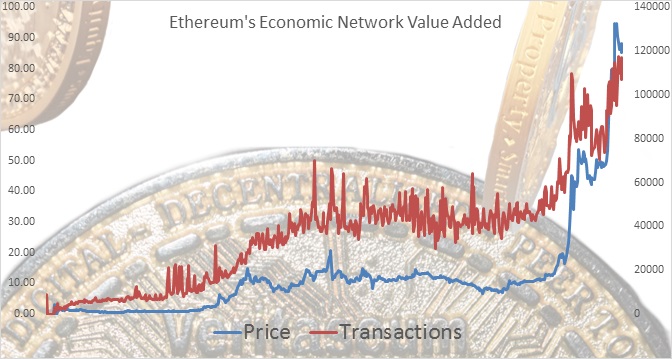

A significant portion of economic value of companies such as Gnosis stems not from traditional operating earnings, but from token value (held on or off balance sheet) appreciation. As the platform matures and transaction volume steadily increases, so does token value. Below is an example of how this as worked on the Ethereum platform, which Gnosis is based upon, and who’s senior board members have founded.

The significant portion of economic revenue that is token appreciation is represented as follows…

-

Valuation

We have assumed that Gnosis is expected to have revenue growth of more than 90.0% in next five years. Based on the Growth Rate Decay Trajectory Method valuation approach, the Value of the Company will range from XXXx and XXXx of the annual revenue. First year (12 months) of the Company is estimated at $X.0 million.

Based on the table below, the value of Gnosis (if it is able to achieve revenue of $x.0 million and rate of growth in annual revenue of 90% and above) can range between $xx.x million to $xxx million.

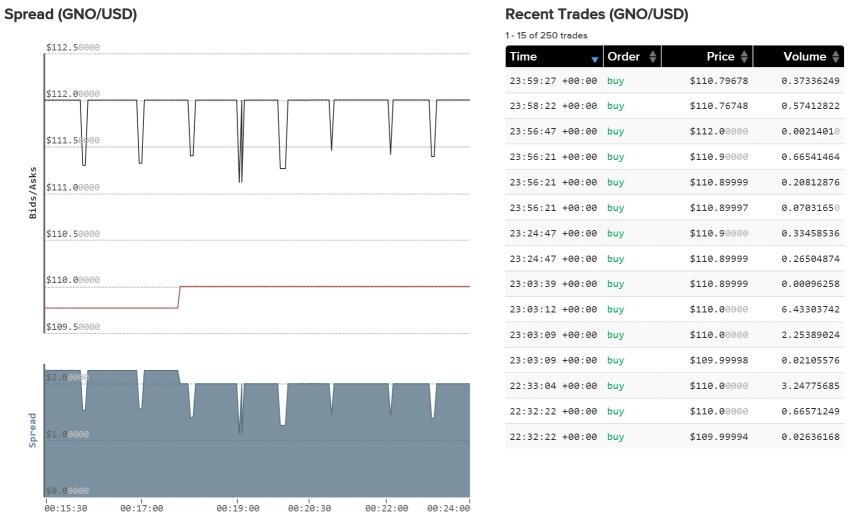

For the sake of reference, recent GNO trading prices, spreads and volume from Kraken....

Disclaimer

Veritaseum, Inc. analysis and conclusions in this presentation are based on publicly available information. Veritaseum, Inc recognizes that there may be confidential information in the possession of the Companies discussed in the presentation that could lead these Companies to disagree with Veritaseum, Inc.’ s conclusions. The analyses provided may include certain statements, estimates and projections prepared with respect to, among other things, the historical and anticipated operating performance of the Companies. Such statements, estimates, and projections reflect various assumptions by Veritaseum, Inc concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies and have been included solely for illustrative purposes. No representations express or implied, are made as to the accuracy or completeness of such statements, estimates or projections or with respect to any other materials herein.

Actual results may vary materially from the estimates and projected results contained herein. Veritaseum, Inc and its affiliates may own investments that are bullish or bearish on the subject entity in this material. These investments may include, but are not necessarily limited to credit-default swaps, equity put or call options, common or preferred equity, warrants and short sales of common stock. Veritaseum, Inc is in the business of advising on, building, consulting for and trading - buying and selling - public and private securities and digital assets. It is possible that there will be developments in the future that cause Veritaseum, Inc to change its position regarding the Companies and possibly increase, reduce, dispose of, or change the form of its investment in the Companies.

This information and work is copyrighted.